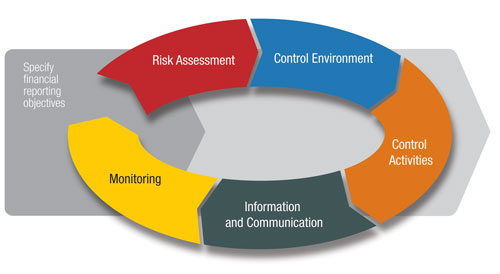

On May 14, 2013, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) issued its final revised “Framework” for internal control reporting. Many accountants and other readers may raise the question, who is COSO and what do they do? Yes, accountants are quite familiar with guidance issued by the Financial Accounting Standards Board (FASB), the Securities and Exchange Commission (SEC), and other standard-setters, but COSO is not a standard-setter. So, this latest version of the COSO Framework arguably is a “sleeper” when it comes to guidance that may affect accountants.

Read More

Tags:

Corporate Governance,

Business & Legal,

SEC,

Accounting & Tax,

Lease Accounting,

Audit Standards,

Accountants

Actions by the SEC, other federal agencies and the courts continue to change or propose changes to the rules concerning the disclosures that publicly listed companies must make. They are responding to the latest series of U.S. federal laws aimed at improving corporate accountability and enhancing growth in a slow economy. Most recently, a court has vacated the SEC rule on disclosure of payments by resource extraction issuers, and the U.S. Government Accountability Office (GAO) has recommended further disclosures about auditor attestation, as follows:

Read More

Tags:

Corporate Governance,

Business & Legal,

SEC,

Audit Standards

The Securities and Exchange Commission (SEC) was created 80 years ago to protect investors, while also nurturing the growth of efficient and transparent markets for securities. Over the intervening years, the balance between protection and growth has shifted many times, leading to many sets of requirements with conditions and exemptions to parse in order to determine entrepreneurs’ notice and filing requirements, and the range of investor opportunities and protections.

Read More

Tags:

Corporate Governance,

Business & Legal,

SEC

One of the Dodd-Frank Act’s many directives to the Securities and Exchange Commission (SEC) was to require annual disclosures by publicly listed “resource extraction issuers” of payments they make to the U.S. federal government or foreign governments, related to commercial development of oil, natural gas, or minerals. SEC thought it met this directive when it issued Rule 13q-1 and associated Form SD in August 2012. However, on July 2, 2013 a federal judge decided that SEC misapplied its authority, and so vacated these provisions and remanded the issue to SEC to try again (American Petroleum Institute v. SEC). Since Dodd-Frank required issuer reporting to begin no less than one year after SEC issued rules, the issuer reporting requirement is now on hold—but the statutory requirement remains in place so further rulemaking should be expected.

Read More

Tags:

Corporate Governance,

Business & Legal,

SEC,

International,

Health & Safety,

Environmental,

Greenhouse Gas,

ghg,

fracking,

hydraulic fracking

On July 1, 2013, the FASB issued three proposals designed to reduce the complexity of certain accounting requirements for private companies. While that is certainly the intent, some unintended consequences may result as discussed below.

Read More

Tags:

Business & Legal,

SEC,

Accounting & Tax,

Accountants,

US GAAP,

GAAP

As mentioned in my September 2012 blog article, “Possible New Lease Accounting Rule—An Update,” a new proposal for lease accounting was likely to “hit the streets” sometime in 2013. Sure enough, a new proposal was issued on May 16, 2013. This proposal was issued jointly by the U.S. accounting standard-setter, the Financial Accounting Standards Board (FASB), and the International Accounting Standards Board (IASB), which issues accounting standards that are used by many companies in countries outside the United States. The two boards are striving to conform their accounting principles and this lease project is one example of that effort.

Read More

Tags:

SEC,

Accounting & Tax,

Lease Accounting,

Accountants

The latest regulator to establish a formal policy offering companies incentives to self-police is the Public Company Accounting Oversight Board (PCAOB), which regulates the accountants that audit the books for public companies and broker-dealers and help prepare their periodic reports. On April 24, PCAOB issued its “Policy Statement on Extraordinary Cooperation in Connection with Board Investigations.” This Policy Statement formalizes guidance to auditors, explaining how PCAOB’s inspection and enforcement personnel view regulated entities’ willingness to go beyond mere compliance, by taking steps such as:

Read More

Tags:

Business & Legal,

SEC,

Accounting & Tax,

Accountants

The accounting standard-setter for companies in the United States, the Financial Accounting Standards Board (FASB) is celebrating its 40th anniversary this year—and for all 40 years of the FASB’s existence, I have been practicing as a certified public accountant (CPA), both in public and industry accounting. I currently author this blog and work on a consulting basis with companies to help them understand the accounting rules as well as the way in which they are developed and issued by the FASB and other standard-setters. From this perspective, I will provide a mix of historical facts and some of my own personal views on the development of U.S. accounting rules.

Read More

Tags:

Corporate Governance,

Business & Legal,

SEC,

Accounting & Tax,

Audit Standards,

Accountants,

AICPA

During annual meetings, corporations consult with their stockholders about recent accomplishments, and seek approval for a range of future activities. Shareholders who don't attend still have the right to participate—in order to vote on pending issues they may assign proxies to vote on their behalf, to corporate management or other parties. State corporation laws and individual corporate charters and bylaws provide standards for proxies and proxy solicitations (many are based on the Model Business Corporation Act, section 7.22). In addition, a corporation that is publicly traded on a national securities exchange must comply with proxy rules issued by the U.S. Securities and Exchange Commission (SEC).

Read More

Tags:

Corporate Governance,

Business & Legal,

SEC

The Financial Accounting Standards Board (FASB) has recently clarified certain guidance relating to not-for-profit (NFP) entities. Specifically, it has issued Accounting Standards Update (ASU) No. 2012-05, Statement of Cash Flows (Topic 230), Not-for-Profit Entities: Classification of the Sale Proceeds of Donated Financial Assets in the Statement of Cash Flows, and ASU No. 2013-06, Not-for-Profit Entities (Topic 958), Services Received from Personnel of an Affiliate. The latter ASU was issued on April 19, 2013. Separately, the American Institute of Certified Public Accountants (AICPA) in March 2013 issued new guidance in the form of an updated Audit & Accounting Guide (AAG), Not-for-Profit Entities.

Read More

Tags:

Business & Legal,

SEC,

Accounting & Tax,

Lease Accounting,

Audit Standards,

Accountants,

GAAS,

GAAP